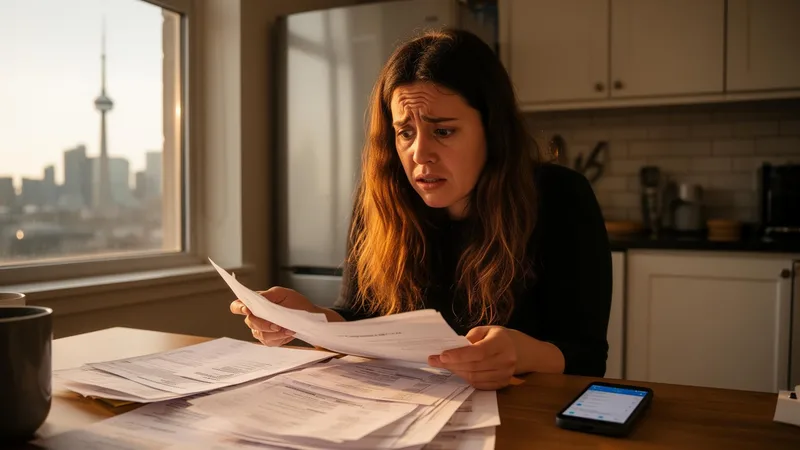

No one schedules a financial inconvenience. It just arrives. Usually with poor timing and dramatic flair.

The car starts making a noise that sounds expensive. The dog needs emergency treatment on a Sunday. The rent comes out the same week your phone screen shatters. The kind of week that makes you stare at your banking app like it personally betrayed you.

For many Canadians, surprise costs are less about bad planning and more about modern reality. Groceries cost more. Utilities climb quietly. Everyday life has become strangely premium-priced. Even people who budget carefully can get blindsided by a single unexpected bill.

The good news: panic is not the only option. There are practical ways to handle short-term financial pressure without creating long-term chaos.

First, pause before you fix it

Urgency can make people choose the loudest solution, not the smartest one.

When money stress hits, there is often an impulse to react immediately. Put it on a credit card. Borrow from the wrong person. Ignore the bill and hope it becomes philosophical instead of real.

A better move is to take one hour and assess the situation clearly:

- How much is actually needed right now?

- Is the expense urgent, or just annoying?

- Can the payment be split or delayed?

- What money is coming in next?

- What option costs the least over time?

That small pause can save a lot of regret.

Cut the drama, keep the priorities

When cash is tight, priorities matter more than perfection. Focus first on essentials:

- Housing

- Utilities

- Food

- Transportation

- Required medical costs

- Childcare

- Time-sensitive repairs that affect work or safety

This is not the week to emotionally support yourself through random online shopping. Your future self has enough character development already.

If needed, delay non-essential spending temporarily. Streaming subscriptions, impulse purchases, takeout habits, and tiny treats can quietly become a large line item.

Check flexible payment options

Before borrowing anything, ask whether the bill itself can be managed differently. Many service providers offer:

- Payment arrangements

- Due date adjustments

- Partial payments

- Temporary hardship options

This can apply to utilities, medical invoices, internet bills, and even some repair services. A surprising number of people never ask. A surprising number of companies will work with you if you do.

Use what you already have

Sometimes the fastest solution is hiding in plain sight. Look at:

- Unused gift cards

- Reward points

- Items you can sell locally

- Tax refunds coming soon

- Money owed to you

- Small subscriptions you forgot existed

- Extra shifts or freelance work available this week

None of these are glamorous. Neither is financial stress. We work with the tools available.

When borrowing makes sense

There are moments when borrowing can be a reasonable bridge, especially when the cost cannot wait and the alternative creates bigger damage. Examples include:

- A car repair needed to get to work

- Emergency travel

- Urgent home repair

- Essential bill payments that prevent penalties or shutoffs

- Temporary cash flow gaps between paydays

The key is borrowing with intention, not desperation. That means understanding repayment terms, total cost, and timeline before agreeing to anything. If you need a fast digital option, some Canadians use platforms like GoDay to explore online loan application options from home. The smartest borrowing decision is usually the one you can realistically repay without wrecking next month.

Avoid the shame spiral

Money stress often comes with unnecessary self-judgment. People think: I should have been more prepared. I'm bad with money. No one else deals with this. None of that helps pay the mechanic.

Unexpected costs happen across income levels. They happen to organised people, messy people, spreadsheet people, and people who keep receipts in a kitchen drawer labelled later. Treat the problem like a logistics issue, not a character flaw.

Build a tiny emergency buffer later

If this season feels financially tight, full emergency-fund lectures can sound insulting. So start smaller. Try building a life-happens fund with manageable goals:

- $100

- Then $250

- Then $500

- Then one week of expenses

Small savings still create breathing room. Even a modest buffer can turn a future crisis into an inconvenience. Progress counts, even when it looks unimpressive on paper.

Talk about money more honestly

Many people stay silent until stress becomes severe. Quiet shame delays practical help. Talk with a partner. Ask a provider for options. Reach out to family if appropriate. Review numbers honestly instead of avoiding them. Financial pressure grows in secrecy and shrinks under direct light.

Final thought

Surprise expenses are part of adult life's least popular subscription plan. They show up uninvited, often expensive, rarely convenient. But one difficult week does not define your finances. A temporary shortfall is not permanent failure. With clear thinking, realistic priorities, and the right short-term tools, you can handle the hit and move forward without turning one problem into three.